Login

LoginMay 09, 2025

Credila vs. SBI Education Loan for Abroad: Which one is the Best?

Have you ever wondered how so many Indian students are able to study abroad each year? For many, overseas education loans make it possible, turning the dream of attending foreign universities into a reality.

When it comes to education loans for studying abroad, two names often come up: Credila (formerly HDFC Credila) and the State Bank of India. Both offer specially designed loan packages to help students with big dreams but limited funds. However, deciding between the two isn’t as simple as it sounds.

In the following comparison, we'll look closely at what Credila and SBI offer. In simple terms, we'll explore their loan features, interest rates, and repayment options. Time to examine the details closely!

Credila vs. SBI Education Loan for Abroad: A Quick Overview

About Credila Loan for Abroad Studies

HDFC Credila education loans is tailored for Indian students aspiring to study abroad. You can apply for the loan even before finalizing your study destination, although the approved amount will depend on the country you select. With its personalized financial solutions, the bank stands out as an excellent option for students enrolled in various programs at more than 1,000 institutions across 35+ countries.

About SBI Education Loan for Abroad

SBI offers the Global Ed-Vantage scheme for overseas education loans, which features a faster online application process, attractive interest rates, and higher loan amounts. In addition to the mandatory education costs, this loan scheme also covers the purchase of study material, laptop, and other essential expenses needed for course completion. Let’s move forward to explore their key features and what they have in common and how they differ.

Repo Rate Cut Leads to Lower Interest Rates on SBI Education Loans

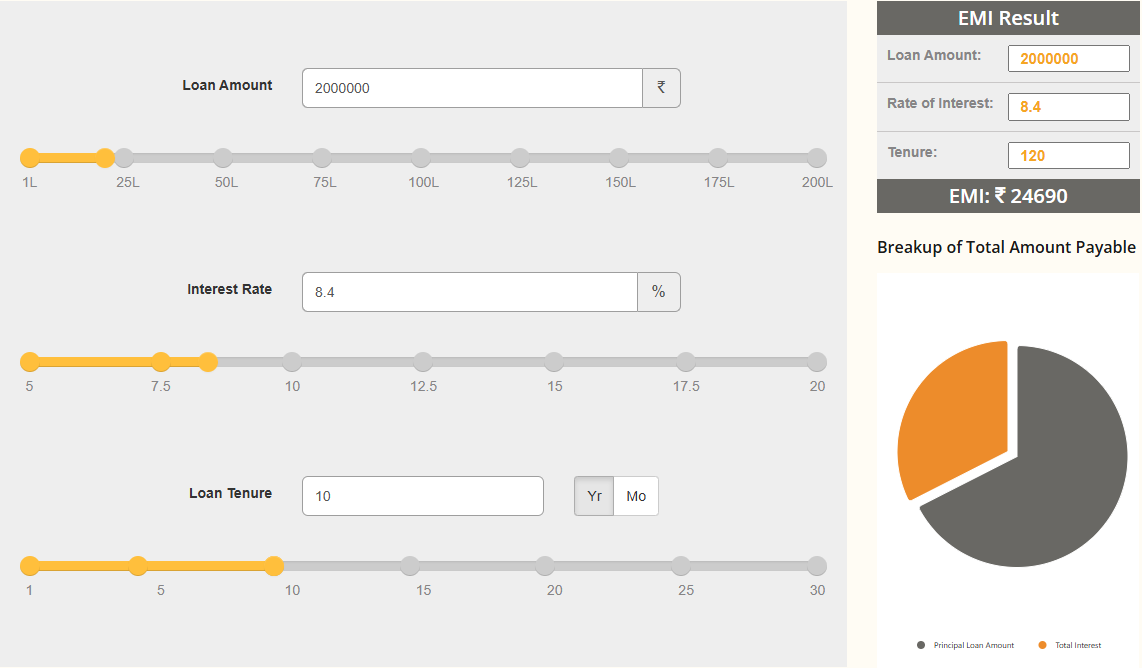

State Bank of India Abroad Education Loan EMI calculator

Calculate How Much You Can Save!

With a loan amount of Rs.20 lakh, an interest rate of 8.4%, and a 10-year tenure, your approximate monthly instalment comes to Rs.24,690.

Credila vs. SBI Education Loan for Abroad: Key Features Comparison

State Bank of India is governed by central authorities like the Reserve Bank of India, while Credila holds the distinction of being India’s first dedicated education loan company. This section compares the relevant features of these two prominent financial institutions, helping you determine which one best fits your needs.

|

Feature |

Credila |

State Bank of India |

|

Loan Amount |

|

Secured Loan up to INR 3 Crore |

|

Interest Rate (ROI) |

For Unsecured Loan between 11.5% to

12.75% |

Basic ROI of 8.40% Concession of: 0.50% for Girl Child |

|

Funding & Margin |

100% Funding |

90% + 10% for Non Premier List for

Universities |

|

Processing Time |

7-10 working days |

20-25 days |

|

Sponsors |

Parents, Grandparents, Immediate

Family |

Parents, Grandparents, Immediate Family,

Family Friends |

|

Study Level & Courses |

Secured Loan for all level of courses Unsecured Loan only for Masters |

Secured Loan for all courses No Loan for UG Diploma/Certificates Courses |

|

Moratorium Period |

Course Duration + 12 months |

Course Duration + 12 months |

|

Repayment Tenure |

12 years including Course Duration |

15 years |

|

Interest Serving |

Serving Simple or Partial Interest during

the Moratorium Period is mandatory |

Serving Simple Interest is optional |

|

Acceptable Property |

Loan on Residential Flat, House,

Shop, Commercial Property *No Loan on Open Plot |

|

Having understood the similarities and differences in the key features of Credila and SBI education loans for abroad, we move onto the next part.

Credila vs. SBI Education Loan for Abroad: Eligibility Criteria

Understanding the requirements is essential for determining your eligibility and ensuring a smooth application process. So, let’s get to that.

Credila

Given below are the criteria to be followed with Credila Loan for Abroad Studies:

-

Both the applicant and the co-applicant must be Indian citizens.

-

Co-borrowers are required to hold an active account with any Indian bank.

-

The applicant must have a confirmed admission before the loan can be disbursed.

Additionally, the applicant & the co-applicant must meet Credila’s credit and underwriting criteria as applicable.

State Bank of India

Here are the SBI Education Loan Abroad eligibility criteria to be followed:

-

The applicant must be an Indian citizen.

-

The applicant must have secured admission to a recognized foreign institution.

-

The applicant or co-applicant must have collateral security to pledge.

Additionally, applicants must adhere to the guidelines set by SBI concerning age, academic background, and more.

Moving on to how you can choose the right bank as per your requirements.

Credila vs. SBI Education Loan for Abroad: How to Shortlist the Right Bank?

Choosing the right bank for your overseas education loan involves considering your academic background, financial requirements, interest rates, and the availability of collateral.

Both offer distinct advantages tailored to diverse needs. For instance, Credila offers secured and unsecured loans, whereas the SBI student loan interest rate is more competitive due to various concessions.

If you're still unsure about making a choice, Élan Overseas Education Loans is here to guide you. We specialize in understanding your preferences and requirements to offer personalized recommendations. Whether it’s Credila, SBI, or another financial institution, we’ll assist you in selecting the option that suits you the best.

So, why wait? Reach out to our team today and take the first step towards your educational journey!

Articles on Overseas Education Loans

Education Loan for Abroad Education at the Lowest Interest Rate

Two students can borrow the same education loan amount to study abroad...Aug 01, 2026

Abroad Education Loan for Diploma Programs

Some of you may not be planning to pursue a degree but a Diploma instead...Aug 01, 2026

Avanse Study Abroad Education Loans

Where do you go when you need an instant education loan to study abroad?...Aug 01, 2026